Observations on December stock and bond markets

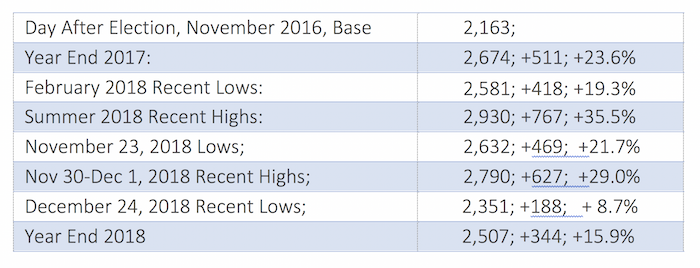

The chart below sets out a few price points for the S&P 500 index since Donald Trump’s 2016 election (point and percentage increases calculated from November 9, 2016).

A few comments from these figures:

- The December 24th low is 19.8% below the September (“Summer” in the chart above) 2018 all-time high, just less than the 20% that constitutes a “bear” market;

- The December 24th low is 12.1% below the year-end 2017 figure, and year-end 2018 is 6.2% below year-end 2017, the first significant down year for the S&P 500 since 2008;

- Note also that the recent high at the end of November (including December 3rd), which showed a gain for the year of 4.3%, was erased during December;

- As for the somewhat longer view, the index remains positive, at 15.9% for the two-plus years since the election, albeit well below the levels reached in September and November of 2018.

A recent NY Times article (NYT, 12/27/18, page B1) about a particularly volatile day, when the S&P was down 60 points (almost 3%) but finished up 20 points (just under 1%), described the current climate as follows:

“Investors have struggled to find their bearings this month as the S&P 500 hurtled toward bear market territory, defined as a 20% drop from a recent high point. They are trying to assess the prospects for economic growth and corporate profits as interest rates rise and a trade war with China persists, while most recently factoring in internal White House turmoil and the President’s antipathy toward the Federal Reserve Chairman… Stock swings (aka volatility) have been larger and more frequent than at any other time since 2011. On 15 days in 2018, the value of the S&P 500 changed more than 3 percent, which did not happen at all in 2017 and on only five days in 2016. In 2011 that figure was 24 times… Traders have their own concerns with Mr. Powell (Fed Chairman) as well… Investors are concerned the Fed might not be willing to change plans for further increases in interest rates even if market turmoil persists.”

We reference this article in making some observations of our own:

- The article, to its credit, specifically links the current issues to prospects for economic growth and corporate profits. It does not, however, explain why these issues, well known for some time, became such problems during October and then again in December.

- What is not mentioned is that the recent declines in the S&P 500 index have reduced the price (“P”) portion for the index, so that its P/E (“price/earnings”) ratio, which reached approximately 25 during the highs of 2018, has declined to approximately 19 (http://www.multpl.com/, based on trailing 12-month reported earnings). As the P/E for stocks declines, they become more reasonably valued, unless of course the declining prices are correctly foreseeing declines in corporate earnings, which will only be known as the future unfolds.

- Does anyone remember the volatility of 2011, or the underlying events that were cited as factors back then? Note that since the 2008 decline of 38.5%, the S&P 500 index has gained in all years until 2018, except for two years (2011 and 2015) with basically flat results.

- The biggest problem with the article is the lack of distinction between investors and traders. We suspect that much of this volatility is the result of traders trading with each other, using market pricing as the measure of their daily gains and losses. This trading activity does not appear to be based on financial or economic rationales, but rather on an effort to gain from the next, often daily, market price movements… Unlike investors, traders do not have a long-term perspective.

- While the stock market appears to have stabilized in early January 2019, the recent declines can resume at any time, especially in light of ongoing global economic and geopolitical instability. In any case, we continue to advocate for allocations to stocks appropriate to each investor’s situation, and a long-term time horizon when considering what that allocation should be.

Turning to bonds, prices rose in December, as interest rates on the ten-year US Treasury declined for a second consecutive month, this time from 3.0% to 2.77%. This was surprising, because higher interest rates are one of the media’s main reasons for the recent stock market declines, even though stock prices had moved higher through the end of September (note: The Federal Reserve made its fourth quarter-point (1/4 of 1%) 2018 rate increase in December). One explanation is that the ten-year Treasury price is set by market participants buying and selling these bonds, whereas the interest rates the Fed controls are overnight rates charged to banks (ultra-short term), which the Fed uses to try and modulate inflation rates and economic growth. There are times when there is a divergence in the direction between these two rates, and if the ten-year rate gets close to the short-term rate, some market observers believe that is a signal for an economic slowdown. In any event, for now, the allocation to bonds in investor portfolios is providing positive returns to offset at least some of the stock declines.

NOTE: Any recommendation contained in these Comments may not be suitable for all investors. Moreover, although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Past performance may not be indicative of future results. It should not be assumed that the future performance of any specific investment or strategy will be profitable or equal to past performance levels.